INDEPENDENT BANK (INDB)·Q4 2025 Earnings Summary

Independent Bank Corp Q4 2025 Earnings: EPS Beat, NIM Expansion Continues

January 23, 2026 · by Fintool AI Agent

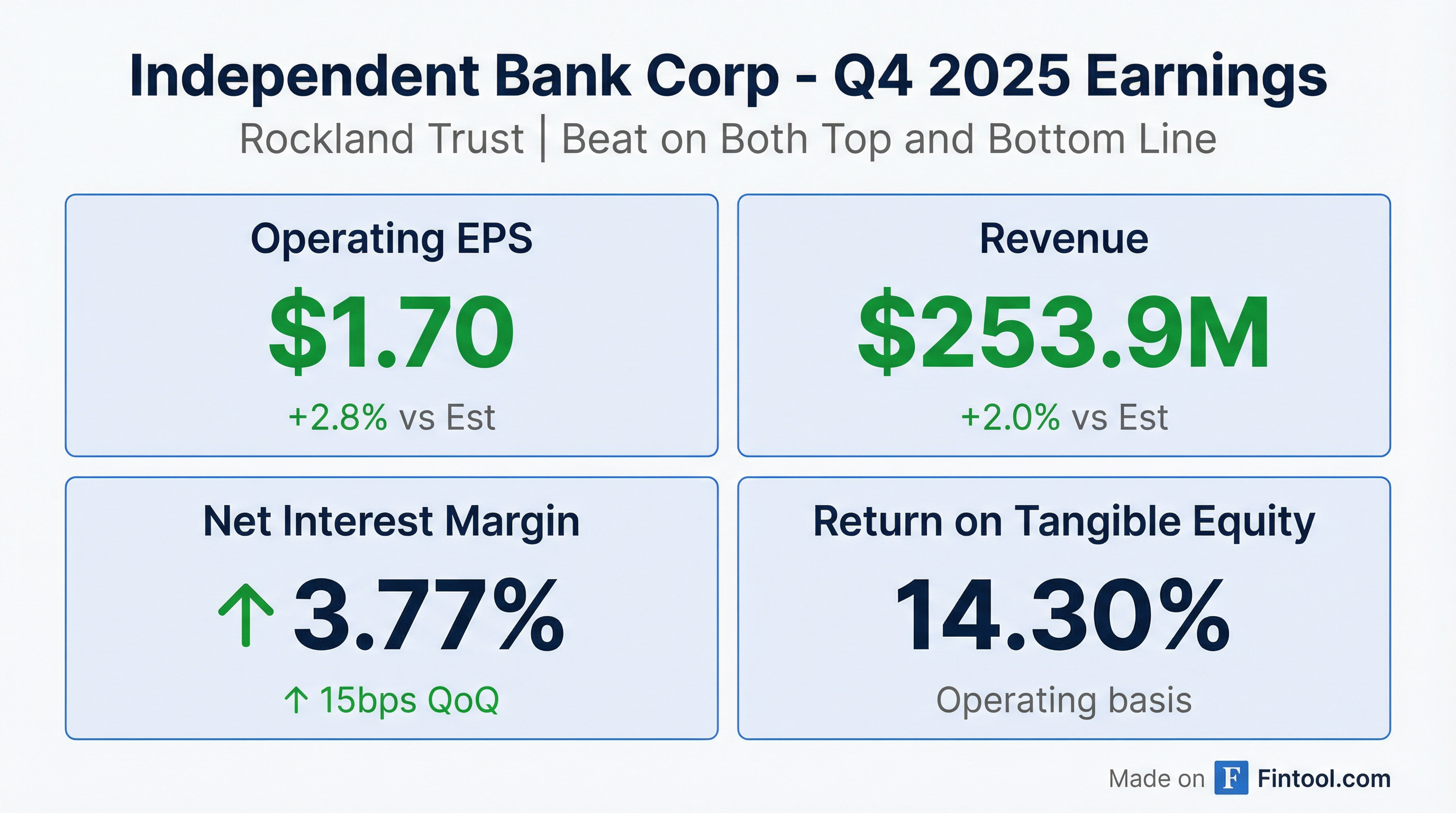

Independent Bank Corp (INDB), parent of Rockland Trust, delivered a solid Q4 2025 with beats on both EPS and revenue. Operating EPS of $1.70 topped consensus by 2.8%, while revenue of $253.9M exceeded expectations by 2.0%. The quarter capped a transformative year that included the successful integration of Enterprise Bancorp and a 60% increase in operating EPS from Q1 to Q4 2025.

Did Independent Bank Corp Beat Earnings?

Yes — beat on both lines.

Operating results excluded $12.3M of merger-related expenses from the Enterprise acquisition.

Profitability Metrics

The NIM expansion was driven by a 12 basis point reduction in deposit costs to 1.46%, translating to roughly 30% deposit beta on the Fed's 40 bps of cuts during the quarter.

How Did the Stock React?

Down 2.2% despite the beat, closing at $78.75.

The sell-off appears driven by profit-taking rather than fundamentals. INDB has rallied over 50% from its 52-week low of $52.15, and shares traded near their 52-week high of $80.92 heading into the print.

Historical Earnings Reactions

What Did Management Guide?

Management established two primary profitability targets for Q4 2026:

Full 2026 Guidance

CEO Jeff Tengel emphasized a "hold-the-line mentality" on staffing and disciplined expense management heading into 2026.

What Changed From Last Quarter?

Enterprise Integration Complete ✓

Six months after closing the Enterprise Bancorp acquisition, management declared integration substantially complete:

- Commercial banking: ~100% retention of client-facing personnel, negligible customer loss

- Retail banking: All 12 Enterprise branches retained, 95%+ deposit retention across all branches

- Wealth management: Retained "almost all" targeted employees

- Cost saves: Full realization of acquisition synergies

The next milestone is a core system conversion scheduled for October 2026, pushed from May to allow more preparation time.

Credit: "8th or 9th Inning" of Cycle

Management expressed confidence credit issues have peaked:

The uptick in NPAs was driven by one $18.1M office loan that is now under a purchase and sale agreement with ~$2M of loss already reserved.

One additional $9.9M criticized office loan was impacted by GSA lease pullbacks related to DOGE initiatives, though the property remains current and cash flowing.

Capital Deployment

Management acknowledged capital levels exceed internal targets and committed to returning excess via buybacks:

In Q4, the company repurchased 548,000 shares for $37.5M at $68.39 weighted average price. Full year 2025 buybacks totaled $61M (913,000 shares).

Key Management Quotes

On profitability improvement:

"Between the first quarter of 2025 and the fourth quarter of 2025, our operating EPS increased by 60%, our operating ROAA rose by 40 basis points, and our operating ROTC improved by 529 basis points." — Jeff Tengel, CEO

On M&A appetite:

"We're really not focused on M&A at the moment. The priorities are organic growth, watching our expenses, and focused on the conversion that's coming towards the latter part of the year... You don't get a second chance if you don't [get it right]." — Jeff Tengel, CEO

On credit cycle:

"I would say we do think we're at the peak or pretty close to the peak... like the 8th or 9th inning." — Jeff Tengel, CEO

Loan and Deposit Trends

Loan Composition Shift

The bank continued its strategic pivot toward C&I lending:

Commercial loan closings reached $789M in Q4 (up from $754M in Q3), with 52% of fundings in C&I. The middle market team represented 27% of closed commitments.

Deposit Franchise Strength

Management highlighted deposit beta management: ~5-10% beta on small-balance "rack rate" deposits, 70-80% beta on rate-sensitive exception-priced deposits, blending to ~20% overall.

Analyst Q&A Highlights

On deposit betas (Mark Ruggiero, CFO):

"We have really good visibility into a lot of the small balance core deposits that we don't move a lot on... We're probably only in a 5%-10% beta in that bucket, but it's the higher rate, more sensitive, where we do very deliberate exception pricing, and that's the bucket where we typically are seeing 70%-80% betas."

On securities portfolio (Mark Ruggiero, CFO):

"Of the $670 million [repricing], $625 million of that is yielding about 1.80% today. If we're conservatively assuming to put that back into 4% securities, that's a nice lift to the securities book throughout 2026."

On AI investments (Jeff Tengel, CEO):

"We'd rather get two or three wins, knowing that it got done correctly and we got the output that we were looking for, than try and do 25 of these in each business unit kind of doing it themselves."

Forward Estimates

Values retrieved from S&P Global

The Bottom Line

Independent Bank Corp delivered a clean beat in Q4 2025, capping a year of significant operational improvement. The Enterprise integration is behind them, credit appears to be peaking, and NIM expansion has further room to run as low-yielding securities reprice higher. The 2026 roadmap is straightforward: organic growth, expense discipline, capital returns, and executing the October core system conversion without disruption.

The stock's 2.2% decline on strong results likely reflects elevated expectations after a 50%+ rally from lows rather than any fundamental concern. With forward estimates calling for continued EPS growth through 2026 and management targeting 15% ROTCE, the setup remains constructive for patient shareholders.

Related Links: